Recently, Groundfloor crossed another important milestone, repaying our 100th loan in January. We passed that milestone realizing no loss of principal in three years of lending. In one case of a loan we made two years ago, we were unable to recover the full interest due. We go to great efforts to protect our investors’ capital, and have prided ourselves on a spotless record of always returning it. Paying back loans is our job. That’s what we do for a living.

Today, our undefeated record sees its inevitable end. We are reporting our first loss of principal on a loan and a return without interest on another. This post covers the full details of what went wrong with these two separate, but related, new construction loans made in Dallas, Georgia to a single borrower in November 2015 and March 2016.

We’re not the kind of company who sweeps its problems and shortcomings under the rug. When results do not meet our expectations, we make a point of studying why. We share our findings openly with our stakeholders without excuse, and commit ourselves to improving. No other company in the peer-to-peer lending space does this. Let’s get to it.

The Loans

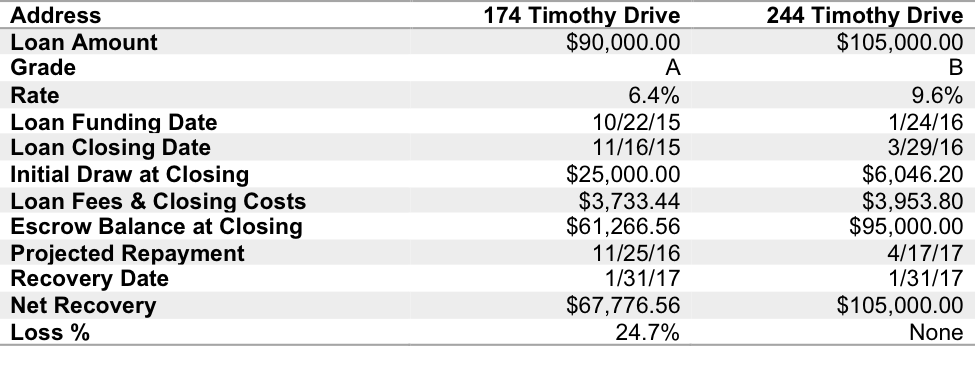

The loans for 174 Timothy Drive and 244 Timothy Drive were originated to finance the construction of one single-family house at each address. Repayment was expected through a sale of the property upon completion of construction.

What Went Wrong

Groundfloor has completed an internal review of both loans to establish the causes of the loss on 174 Timothy Drive and the lost interest on 244 Timothy Drive. We have identified five factors:

-

At the time the loans were granted, Groundfloor did not have a borrower concentration policy in effect. Accordingly, the Timothy borrower obtained multiple loans before establishing a positive repayment history with Groundfloor. The Timothy Drive loans were the 3rd and 4th of the borrower’s four Groundfloor loans. The borrower’s financial troubles (see below) had a collateral effect on all of his loans with us.

-

The property values utilized in underwriting these loans were based upon borrower submitted comparable sales. Full appraisals would have included independently identified comparables, as well as detailed supply and demand analyses to further support the concluded value. Loan-to-Value is a significant driver in Groundfloor’s proprietary credit model, so the value assigned to the underlying collateral may have resulted in a higher than appropriate rating.

-

While all real estate investing involves significant risk, land development and new construction present particular risk in that site conditions may not actually be known until construction commences. The Timothy Drive sites were subject to latent geotechnical issues that significantly increased the cost to install an appropriate septic system.

-

The initial draw on each loan should have been withheld until the borrower provided evidence that permits had been obtained for construction of the houses, including construction of the associated septic systems.

-

The construction budgets provided by the borrower lacked sufficient detail and did not include a contingency for latent conditions. As such, we were reliant upon the borrower funding construction overruns and contingency items personally, not from funds held back in escrow.

Our Asset Management Actions to Prevent Loss

In the months following the closing of 244 Timothy Drive in March 2016, the Groundfloor Asset Management team got actively involved with the borrower with respect to his initial two loans with us. These residential fix-and-flip loans were made on two properties located in Cartersville, Georgia.

The first was a $25,000 loan with a six month term. Proceeds of the loan were to be used for the renovation and sale of a single family home. Although the borrower failed to payoff the loan at maturity, Groundfloor employed proactive asset management to secure full repayment of principal and interest within 10 days of maturity.

This experience prompted us to immediately engage the borrower with respect to his other Groundfloor loans. Another loan of $55,000 for a residential fix and flip was experiencing numerous construction delays. Groundfloor staff met the borrower at the property, conducted an inspection, and determined that the borrower needed more capital and time to complete and sell the property.

Groundfloor entered into a workout agreement to grant a short-term loan extension in exchange for an $8,000 capital infusion by the borrower. Through the course of regular borrower contact, Groundfloor concluded that the borrower was suffering significant financial difficulty. This prompted Groundfloor to seek a global resolution to incorporate all of his outstanding Groundfloor loans.

Pursuant to our asset management procedures, the borrower was put into default, foreclosure action was commenced and discussions were pursued to explore non-foreclosure resolution options. Ultimately, Groundfloor successfully negotiated a title transfer via deed in lieu for all the Cartersville property together with the two Timothy Drive properties. This action saved the time and expense associated with foreclosure. The fix and flip property was sold by Groundfloor within 45 days and investors were repaid full principal and interest.

Upon taking title to the Timothy Drive properties, Groundfloor met with Paulding County Building Dept. personnel to determine the status of the permits for each property. At this meeting Groundfloor was advised that the properties had what is known as a ‘latent condition’ which limited the development of each lot.

The latent condition affecting each property related to the properties being located in an area of shallow bedrock which precluded the installation of a standard septic system. Both properties required the installation of a specialized drip septic system. The cost of this system is at least twice the cost of a traditional system septic system. Further, the County advised that although the borrower had been working with the County and his engineer regarding the installation of the drip system, a permit had not been issued for the septic system or the construction of a house on either property.

The latent condition reduced the value of each property from the value provided by the borrower and also the value determined by Groundfloor. Groundfloor engaged a local broker to assist in determining the revised value and was advised that the properties had a $20,000 market value.

Groundfloor formally engaged the broker to market and sell both properties. The broker secured a buyer for both lots at a combined purchase price of $20,000. The buyer’s offer was subject to due diligence. During the buyer’s due diligence the buyer also contacted Paulding County to understand the latent condition affecting the properties.

The buyer also undertook a survey of the property and uncovered that there was an encroachment into 174 Timothy Drive from the adjacent owner’s septic system. The buyer requested a $5,000 price reduction to reflect the actual site conditions. Groundfloor agreed to this price reduction to $15,000 in the interest of finalizing the transaction and repaying investors in a timely fashion.

The sale of the two lots together closed January 27, 2016. Here is how we tabulated the proceeds:

Allocation of Sale Proceeds: We allocated the proceeds of the $15,000 collected from the sale according to the acreage and the impact of the impairment of 174 Timothy Drive on the property value.

Closing Taxes, Fees & Commissions: We paid $100 in real estate tax for each lot, plus sales commissions of 6% on the sale proceeds as allocated ($255.32 and $644.68 respectively).

Refund of Groundfloor Fees: Although we incurred significant costs well in excess of the servicing revenue due to us, we have forgone our servicing fee of 1.5% of the loan amount on both transactions. In view of the previously unknown problems with 174 Timothy Drive, which are directly linked to the amount of principal loss, we also elected credit lenders with our 2.5% origination fee earned on that loan.

What have we changed?

Since making these loans, Groundfloor has implemented significant improvements to its staff, underwriting and loan servicing to better safeguard investors and align Groundfloor’s lending policy with industry best practice. These improvements can be broken down into three main categories: People, Policy, and Procedure.

People

- In August 2016, Groundfloor’s lending operations team was re-organized to capitalize on the experience and expertise of existing and new team members. All current senior team members have extensive experience with development, renovation and/or commercial real estate lending.

- Groundfloor now has a dedicated asset management team which proactively works with borrowers to ensure development works are proceeding in accordance with an agreed budget and timeline for completion of the works.

Policy

- Borrowers are limited to a maximum of two loans until at least one loan is paid back in a manner acceptable to Groundfloor, subject to case-by-case exceptions following additional diligence and at the discretion of management.

- Groundfloor conducts regular portfolio reviews to identify potential sponsor or market concentration risks.

- Groundfloor has focused its product offering on the residential fix and flip market for the time being.

- Our underwriting process now includes a dual approval sign-off; a practice consistent with industry best practice.

Procedure

- To determine valuations, we are primarily using Broker Price Opinions that we order, and possibly a full appraisal, for all loans. We are moving away from borrower-submitted comparable sales as evidence of as-is or after-repair value.

- The Director of Asset Management reviews all Statements of Work that have a significant construction component to ensure the budget allows for sufficient contingency to ensure borrowers can address latent conditions and other items which may arise during a project.

- An independent inspector certifies the amount of each draw prior to payment being released.

Summary and Conclusion

In summary, we have found some areas where we can improve our process. We also found that risks were proactively confronted and managed as they emerged. We’re better lenders than we were when we first originated the loans in question. As we made improvements, we also took significant steps to minimize the loss and make it right. We hope that’s evident to all.

Fortunately, these two loans have been an exception in many ways. We take the loss seriously, while also putting them in proper perspective. As detailed in our monthly public regulatory filings (the most recent of which you can find here), for the reporting period that ended January 13, 2017 this $22,223 loss represents 0.1% of the $21.0 million of principal and 0.5% of the 199 loans we had originated at that time. This first loan on which we’ve lost principal constitutes 0.2% of the $9.1 million of principal and 1.0% of the 101 loans we had repaid by the time of the report.

Most importantly, Groundfloor continues to deliver an outstanding value for its investors. As the only path for non-accredited and accredited investors alike to participate directly in loans backed by real estate, we’re especially proud of the 15.5% gross return we generated for our investors on average through over 100 repaid loans. Today’s loss bumps that yield down to 15.3%. Through the beauty of theoretical portfolio diversification and hyper-fractionalization made real by Groundfloor’s unique offering model, the median investor in this loan lost just $27.16.

We appreciate the trust and faith of those who have been with us since the early days of our national expansion just over a year ago. And we look forward to growing and welcoming many more investors in the year ahead. As always, whether you invest with us yet or not, we welcome your feedback, critical commentary and suggestions about these loans or any other topic below in the comments, or by email directly to me and Nick at founders@groundfloor.us.