By the 15th of each month, Groundfloor publishes our Asset Management Monthly Update, where we deliver key portfolio statistics from the month prior. While this monthly series primarily focuses on the numbers, we occasionally add commentary on processes, practices and the methodologies undertaken by our Account Management team.

In this blog post, we will take a deeper dive into our Asset Management practices, discuss the team's construct as well as how we manage our active portfolio., Our goal is to foster relationships with Borrowers and proactively address loan performance before issues materialize.

By sharing our approach, we will deliver on our commitment to transparency and earn your confidence in Groundfloor as a company, and the loans we fund and service. Groundfloor continues to deliver strong returns to our investors while mitigating risk and preserving capital.

State of the Union

High interest rates and tighter capital market conditions continue to create challenging conditions for some participants within the real estate finance industry. For others, this environment creates opportunity.

As the first and only provider of primary capital built on a base of pure retail investor capital, Groundfloor is built differently from other platforms that may sound the same but are not. Here’s how we’re different and why that matters when you’re considering where to invest:

Regulatory Innovation

Groundfloor established a unique regulatory position that allows us to offer investments to everyone, regardless of income or wealth--to both accredited and non-accredited investors. The breadth of our capital base makes us more resilient when markets get choppy. Meeting the requirements to build our broad base of capital forced us to be more efficient in every area of our operations.

Direct Capital Supply

Our strong retail investor base provides us with the power to source, process, underwrite and then originate all of the platform investments we offer. We have unfettered control over the projects we fund, the neighborhoods we serve, and the partners we work with.

Self-Origination

We source our own deal flow with product features no other capital provider can match. No third party shapes the deals we see or sets the criteria on which we provide capital. In fact, we’ve adjusted our lending guidelines to safeguard our investors’ capital eight times since the pandemic started. Our retail investor base gives us enormous control and flexibility!

Integrated Asset Management

Groundfloor calls the shots on our portfolio when it comes to monitoring progress, deciding how execution delays or unforeseen issues are resolved. Our experienced Real Estate and Asset Management team is 100% focused on serving the long-term interests of our platform investors.

Accountability & Transparency

With Groundfloor, you’re not investing in a fund but building your own portfolio. That’s why we lead our industry in accountability and transparency. We provide detailed regular reporting on every LRO, publish broad-based analyses of actual performance (e.g. our Diversification Analysis and Loan Grade Analysis and our monthly Asset Management Report including a downloadable CSV file detailing the performance of every repaid LRO repaid), and publicly file our financials with the SEC every six months.

Customer-Owned

In an era when venture capitalists are now calling the shots for startups that they previously overfunded at inflated valuations, it’s especially healthy to be self-funded. Groundfloor’s co-founders have maintained corporate control and shared it since 2018 through a series of public stock offerings with you, our investors. As a result, over two-thirds of the company is owned and controlled by its customers, co-founders, and employees. With ten years of operating history and over $1 billion in investments sold, you can rely on our continuing stewardship.

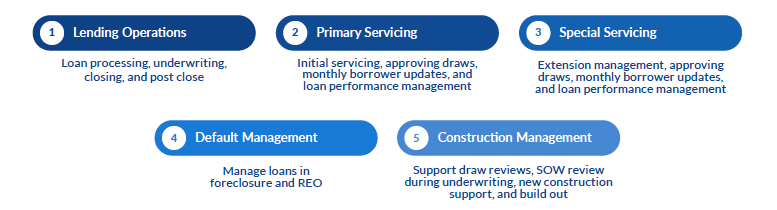

Asset Management Team Construct

Groundfloor invested heavily in people, systems and improved processes to better surveil the market, collateral and partnerships. We formed a new Real Estate group, to roll up to Asset Management and expanded our expertise with two new groups, Default Management and Construction Management.

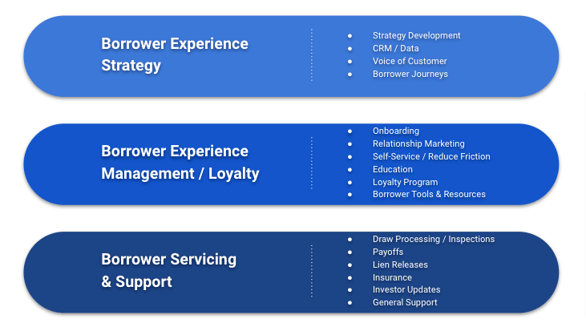

Additionally, we manage a Borrower Experience team, with the following roles and responsibilities:

With new/expanded policies in place, key actions undertaken by the team are:

Early Engagement

- Defined Manager assignment in Primary Servicing

- 120 Days post origination reach outs

- Identify loans with no activity or updates

Routine Follow Up

- Review and reach out for latent draw activity over 60 days

- Occupancy Inspections when funds depleted

Default Action

- Progress Defaults issued when appropriate per loan documents

- Default issued when occupancy violations after inspection confirmation

Forbearance Changes

- Only grant extensions for loans where the project is at least 65% complete and have the greatest potential to repay during the 90 day Forbearance period

- Forbearances maturing are not eligible for an additional extension

- Increased fees for improved response from borrowers

Actively seek bids from Short Sale remedies and distressed asset buyers

- Actively pursue all potential exit strategies for defaulted loan repayment

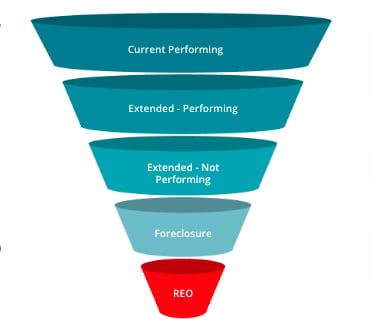

Each day, the Asset Management team is managing the current book of business, with visibility into current Loan Repayment Status or Loan States. While on any given day, the volume of loans within each tier fluctuates, the goal is to maintain the highest number of volume within the Current/Performing state.

We know that while it is ideal to have an active portfolio entirely of Current/Performing loans, that is not reality for Groundfloor, or any other lender.

Overall, Groundfloor believes the mix between those that have Repaid, Current/Performing, and those that are in Default or even REO is healthy

As an investor, understanding the definitions of these terms and understanding how the Asset Management team manages our loans within these states is important.

Repaid Loans - When the borrower has paid back the loan on their property and the interest is distributed back to the investors of the LRO associated with that particular property.

Current Loans - Performing loans with active renovation projects which have corresponding LROs that have been sold on our investment platform.

Extended Loans - Loans where the project completion and/or loan repayment did not happen before the intended maturity date. The borrower continues to work towards completing the project through sale or refinance and will have penalty interest and fees applied.

Defaulted Loans - Loans where Groundfloor's Default Servicing team has engaged with counsel to file legal foreclosure proceedings to take possession of the property as collateral for the defaulted loan.

REO (Real Estate Owned) - Groundfloor takes ownership of the property through the foreclosure process and works to sell the asset in order to recoup as much principal and interest for our investors as possible.

Expanded Commentary on Defaulted Loans

While the term "default" at face value has a negative connotation, the sub-context of loans in this state are not necessarily bad and by no means immediately implies this loan is not performing and investments will be lost.

When a loan is moved into a “default” status, Groundfloor has escalated the servicing to include legal action against the borrower and their entity in an effort to expedite the repayment. Conventional servicing did not produce the results required to repay the LRO and legal action is required to create a sense of urgency with the borrower.

A dedicated Groundfloor Default Servicing Team is deployed to manage communication between the borrower, their representatives as well as foreclosure counsel assigned by Groundfloor. Updates are tracked and updates monthly for investors.

The majority of loans that repay out of default, repay with principal plus interest. Over the past three years 83% repaid with principal or better recovery, 68% of loans repaid from default have done so with a 5% interest or better recovery and 51% have repaid with a 10% interest recovery or better.

Loans will move into "default" for specific reasons. Borrowers inability to complete the project due to, permitting delays, unexpected costs during construction and poor project management are the most common examples of failure to meet the obligations set by Groundfloor.

To combat this, our Construction Management Team positioned to review all Scopes of Work that are submitted for review during the origination process to ensure that budgets meet the required renovations and that our target After Repair Values can be met.

One of the key components of our Asset Management team is communicating with our borrowers. When these legitimate reasons are discussed, we negotiate contractual terms to extend the loans for these very real world scenarios to remedy.

In fact, more often than not, Groundfloor pays back you, the investor, with a higher than expected amount for many loans in default due to the increase in fees, etc.

Special Servicing Process - Foreclosures

The Asset Management team pulls loans flagged as "Extended" that then meet specific criteria. Decisioning criteria for moving a loan into foreclosure occurs across 5 categorical inputs. If a loan meets the foreclosure criteria, key methodologies are undertaken, which include referring the file to an attorney, setting a sale date, providing bidding instructions and moving ahead with the formal REO process.

Conclusion

The feedback and comments received on a monthly basis when we post our latest Asset Management blog have been tremendous. As we continue to track and respond to commentary, for topics that are more relevant to how Groundfloor manages our portfolio, we will opt to update this blog so it can act as a definitive resource guide into policies and practices.