“A loan I invested in went into default. Does this mean I am going to lose my investment?”

This is one of the most common worries we hear from investors, and understandably so. The term “default” typically has a negative connotation, especially for those who remember the 2008 financial crisis. On the GROUNDFLOOR platform, however, a loan in default is not necessarily an indication that the loan is headed for a loss. This blog post will provide a detailed explanation of what a default on our platform actually means and why a loan in default is not necessarily as concerning as one might think.

How Loan Performance Is Defined

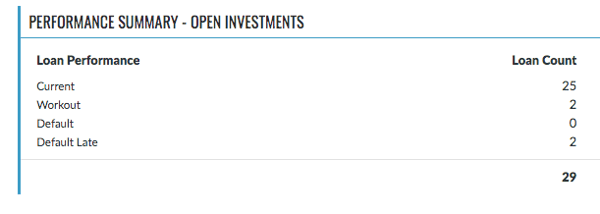

To check on the performance of your open investments, sign into your Investor Account and click on Investment Activity in the dropdown menu, then choose the “Open Investments” tab. Doing so will pull up a chart that looks something like the following:

Open investments are categorized into one of four categories based on their performance. These categories are characterized as follows:

- Current - loan is in compliance with all terms of the loan contract and is progressing according to schedule

- Workout - we have agreed to an extension of the loan term with the borrower

- Default - loan has defaulted on one or more terms of the loan contract, including but not limited to: not repaying the loan by the maturity date, allowing insurance to lapse on the property, not keeping current with tax obligations, missing more than one required payment (if monthly payment loan), or not making scheduled progress on the project

- Default Late - loan has defaulted on one or more terms of the loan contract and the loan has passed the maturity date

How GROUNDFLOOR Manages Defaults

A borrower receives a notice of default when they have not adhered to one or more of the terms of our loan agreement. This can include (but is not limited to) not keeping current with insurance and tax obligations, not providing the requisite updates on project progress, or being 90+ days delinquent on the loan’s monthly payments (if the loan has a monthly payment structure).

Once a borrower receives notice that their loan is in default, they have 30 days to cure the default. If the default is not cured after that 30-day period, GROUNDFLOOR has the option to proceed with foreclosure (provided, of course, that we believe foreclosure to be the best course of action to achieve a satisfactory resolution for our investors). While we always have the right to foreclose on a property, our team strives to use this only as a last resort, as foreclosure processes can be lengthy, costly, and complicated. As is the case with all of our loans, our highest priority is maximizing repayment of principal and interest, while minimizing the time to achieve repayment runs a close second.

For a more detailed look at our Asset Management process, please refer to this blog post.

Loans can move from one performance state to another depending on their specific circumstances. Loans may change performance states in several different ways:

- If a “Default” loan is cured within the 30-day period, the loan will change status from “Default” to “Current” to indicate that it is now in accordance with the loan contract.

- Similarly, a “Default” loan can become a “Workout” loan if we decide the best course of action is to negotiate a modification of the loan’s terms with the borrower.

- A “Default Late” loan can also become a “Workout” loan if we decide the best course of action is to negotiate a modification of the loan term with the borrower.

- Once a loan repays, it is removed from this list (as it is no longer an “open” investment), and it will now appear under the “Repaid” tab in the Investment Activity section of your Investor Account.

What A Default Means For Investors

Seeing a relatively high number in the Default or Default Late categories can understandably cause concern to some investors, but it’s again important to keep in mind that a loan in default does not necessarily indicate that the loan will experience a loss. On the contrary, in the majority of cases, loans in default repay in full, often with higher interest than expected.

How does this occur? When a loan is placed in default, GROUNDFLOOR increases the interest rate charged to the borrower as an additional incentive to get the loan back on track. This heightened default interest rate is then passed along to investors. Thus, though repayment of your investment may be delayed in a default situation, you are compensated for that inconvenience with the additional interest your investment is earning over the default period.

It’s also important to understand that on our platform, a loan in default does not automatically indicate that loss of principal will occur. In fact, according to our analysis of loan performance last year, just 9 loans out of over 340 that repaid in 2019 experienced some degree of principal loss, while 105 loans were able to successfully repay via a workout plan. Our recent analysis of loan performance by grade further reveals that defaulted loans do not always result in a loss; for example, while about a third of C-grade loans originated in Vintage B were labeled default or workout upon repayment, only 1% of all C-grade loans in Vintage B experienced any degree of principal loss. As such, it’s vitally important to understand that labeling a loan as Default is not equivalent to saying that the loan will experience a loss.

It’s also important to note that the chart of open investment performance is dynamic -- it is representative of the state of your open investments at that particular moment. As loans repay or as they move from one category to another as described above, the numbers you see will change; as such, the totals you see one week may not be the same totals you see the following week. To see a more detailed picture of what is happening with any given loan, it’s always a good practice to refer to the investor updates for that loan, which will provide further insight into its progress. Alternatively, you are always welcome to reach out to our support team at support@groundfloor.us to learn more about any specific project.

While loans going into default can often cause investors to feel nervous or worried, we hope the above discussion has helped alleviate any concern about what actually happens in such events. Remember, just because a loan has gone into default does not automatically indicate that it will negatively impact your returns. Our team takes great care to do everything we can to protect the interests of our customers -- whether that’s guiding a borrower to achieve a successful outcome or resolving the problems that customarily arise in real estate investing. As always, please feel free to reach out to us at support@groundfloor.us with any further questions, or drop us a line in the comments.