In this Monthly Market Trends series, we offer you our interpretation of current trends through the eyes of our VP of Market Risk, Patrick Donoghue, and provide you with his balanced commentary so you can make the best investment decisions today for the highest returns tomorrow.

As we enter the spring real estate market, I wanted to check on how the various housing forecasters see housing prices for 2024. These recent forecasts all remain very positive.

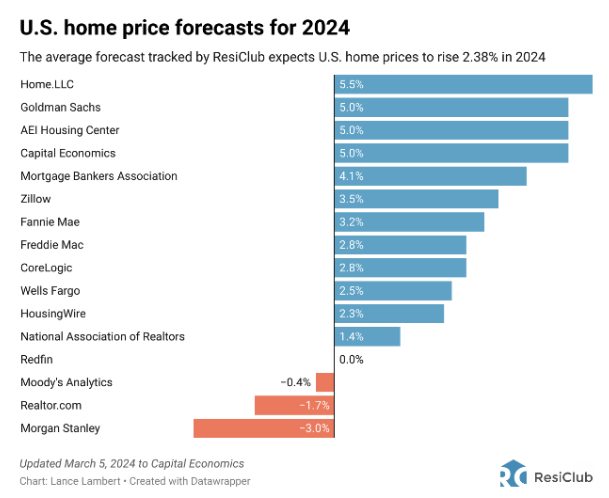

We can observe from the list above that the average estimate of home price appreciation for 2024 is forecast to be 2.4%, relatively in line with expectations that we had at the beginning of the year. It’s important to note that these estimates have remained consistent even though some early inflation readings have come in a touch hotter than expected. Coupling this with seasonal rise in inventory, I maybe would have expected some of these estimates to have wobbled, but they haven’t and that’s a good thing.

I see another bright spot in terms of the spread between the 10-year treasury and the 30-year mortgage. We know that historically, this spread tends to be about 1.75% and that since the Fed began aggressively raising interest rates in Q1 of 2022, the spread has widened to nearly 3%. Well, good news: As of 3/14/24, the spread has come down to 2.57%. Here’s a snapshot of the spread activity over the last year:

When the spread between the 10-year Treasury yield and the 30-year mortgage rate narrows, it typically indicates a decrease in the risk premium that lenders demand for longer-term loans like mortgages.

Here's how it works:

The difference between the yield on the 10-year treasury yield and the 30-year fixed-rate mortgage is a measure of the risk premium lenders require to lend money for a longer period. This spread represents various factors including inflation expectations, economic growth forecasts, and the perceived risk of lending over a longer duration.

When the spread narrows, it suggests that lenders are demanding less compensation for the perceived risks associated with longer-term lending. This could be due to improved economic conditions, lower inflation expectations, or increased confidence in borrowers' ability to repay loans over the long term.

Impact on Mortgage Rates: As the spread narrows, lenders can offer lower interest rates on 30-year mortgages while maintaining their desired profit margins. Lower mortgage rates can stimulate housing demand as they make homeownership more affordable, potentially leading to increased home sales and construction activity.

Lower mortgage rates can also have broader economic effects by encouraging consumer spending on housing-related goods and services. This can contribute to overall economic growth and potentially lead to higher employment levels.

However, it's important to note that various factors influence interest rates, and the relationship between the Treasury yield spread and mortgage rates is just one aspect. Economic indicators, central bank policies, geopolitical events, and market sentiment also play significant roles in determining interest rates.

For Groundfloor borrowers, this means crisper executions on the selling of properties that have been built/renovated because exit capital in the form of 30-year mortgages is less expensive, lowering the affordability gap, and lenders are more willing to take long-term bets on 30-year mortgages because the risk premium has come back in line. For the Groundfloor platform, this means investor capital will increasingly come back as expected, on or ahead of maturity, and platform capital can be recycled in terms of liquidity or future investment.

I vote for future and immediate platform investment. Our automated investment vehicle has been making this long-held vision of Groundfloor a reality, a painless interface, and an easily executable, non-invasive way for everyone to invest in the inflation-hedged, near-equity-like returns our award-winning platform has offered for a decade.

Innovation and critical infrastructure investment into our platform have made the evolution of the mobile investment experience as easy, maybe easier, than ordering a pizza. And I would add that consistent returns in residential real estate are better for you than pizza. So let technology work for you and your portfolio, and check out the automated way you can invest. The platform works for you.

Hats off to my colleagues in the Asset Management group who delivered a great month of repayments in February. If you haven't, check out the Asset Management blog. A lot of internal investment has gone into the development of this group, which includes the Underwriters. Great strides are made daily to improve the experience of borrowers and investors — much sweat! I envision you will see this investment pay off in your account, or maybe you won’t because the repayments into your portfolio will be so easily redirected into new, well-curated residential investments — after your nominated cash builds your liquid position, of course. Okay, I’ll stop. But how can you blame me? I am a believer.

I am also a believer in the positive effects of the narrowing spread I’ve spent much of this blog describing. And you should be too. I promise to stop watching the daily fluctuations of the 10-year treasury if you will.

I will take a deep dive into portfolio returns and loss next month, so I hope you keep reading and thank you for doing so thus far.

Have Questions or Comments?

Please reach out to customer support at support@groundfloor.us or 404-850-9223, Monday through Friday, 9am – 5pm EST.