Welcome to the sixth installment of our Portfolio Analysis, a series we began in January 2018 to provide investors further insight into the performance of our loans over time, and the size and shape of our portfolio of loans outstanding currently.

Since our last installment in this series, an analysis performed as of December 31, 2020, we have seen a significant increase in lending activity, enabled by tremendous growth of our investor base. We have expanded our geographic reach, and have added new channels through which we are able to reach prospective borrowers. And we have achieved this growth without relaxing our underwriting standards or our asset management practices.

The COVID-19 pandemic has brought different challenges to our loan portfolio, and we have responded aggressively and creatively. You can view a summary of how we’ve adapted to the pandemic in this blog post, and you can view a recap of our 2020 performance in this blog post.

Through the challenges, we have continued to monitor our lending practices and outstanding loans rigorously. We continually seek to improve as we scale to meet our investors’ continuing demand for volume, diversification, and returns.

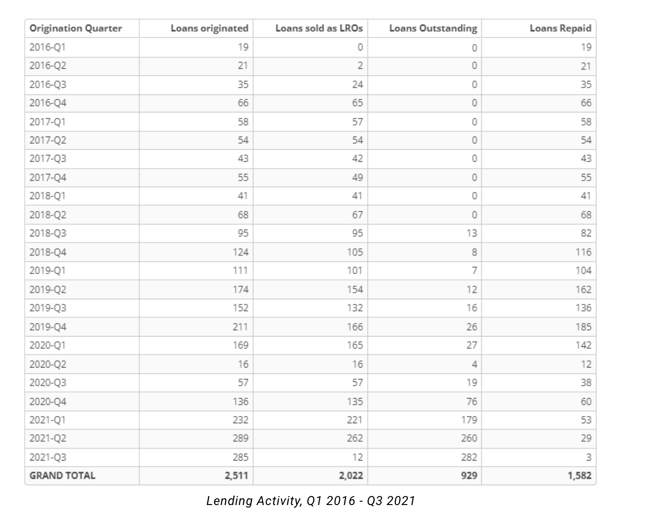

Lending Activity, January 1, 2016 to September 30, 2021

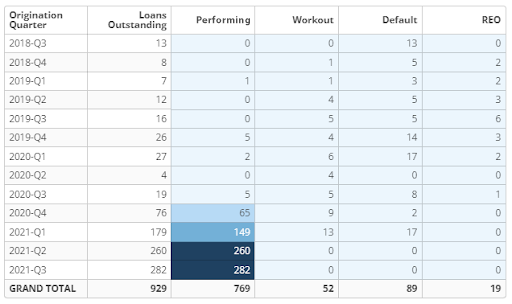

As we have done in prior analyses, we begin by looking at our lending activity over time, organized into “cohorts” of loans according to the quarter in which they were originated. For each cohort, how many loans were originated, how many have since repaid, and how many are still outstanding?

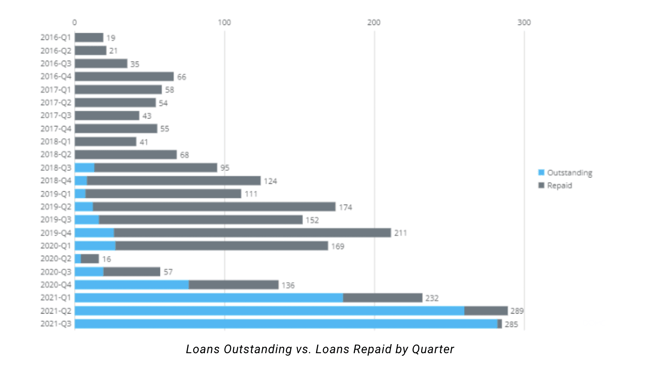

As shown, we have originated (or in a few cases, purchased) 2,511 loans since 2016, and of those, 1,582 have repaid and 929 remain outstanding as of September 30, 2021. After a slowdown in lending activity caused by the disruptions of COVID, our lending activity has returned to its prior growth trajectory, as the graph below indicates.

Repaid Loans, January 1, 2016 to September 30, 2021

Next we turn to an analysis of all loans that have been resolved, whether through successful repayment by the borrower or an alternative means of recovery.

As we did in the previous Portfolio Analysis, we will explore our book of repaid loans by reporting on the “performance state” of those loans at the time of repayment: Performing, Workout, Default, or REO. As a reminder, we have historically defined these performance states as follows:

- Performing – The loan remained current throughout the term of the loan

- Workout – A workout plan was put into effect and the loan was repaid under the terms of the workout agreement

- Default – The loan was put into default by Groundfloor and repaid while in default

- REO – Groundfloor assumed title to the property, either through foreclosure or deed in lieu of foreclosure, and obtained a recovery through sale of the property

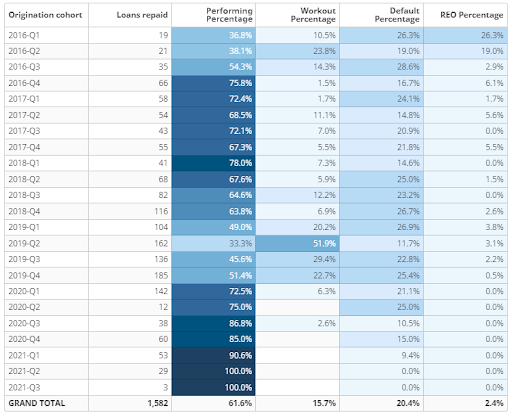

Repaid Loan Performance by Cohort

Repaid Loan Performance by Cohort

The chart above illustrates the impact of COVID-19 on our portfolio. The loans originated throughout 2019 – projects in progress at the time the pandemic swept the United States – experienced the greatest shock. The pandemic economy disrupted the market for housing, for materials, and for construction and renovation services. Regulations and social practices introduced as safety measures disrupted the labor supply and introduced a new source of friction for our borrowers. And state and local government entities have shut down for periods, faced severe resource constraints, and been unable to provide in a timely manner the services (permitting, for example) that are key to keeping the real estate market moving.

As discussed in this blog post, we worked on a loan-by-loan basis to assess our portfolio and take the actions that we believed would maximize the return on our loans. In many situations, we offered our borrowers extensions to allow them the time and flexibility needed to complete their projects and repay our loan, resulting in an increase in workout arrangements for loans originated in 2019, as seen in the chart above. In others, we accepted negotiated loan repayments that we believed maximize our investors’ return.

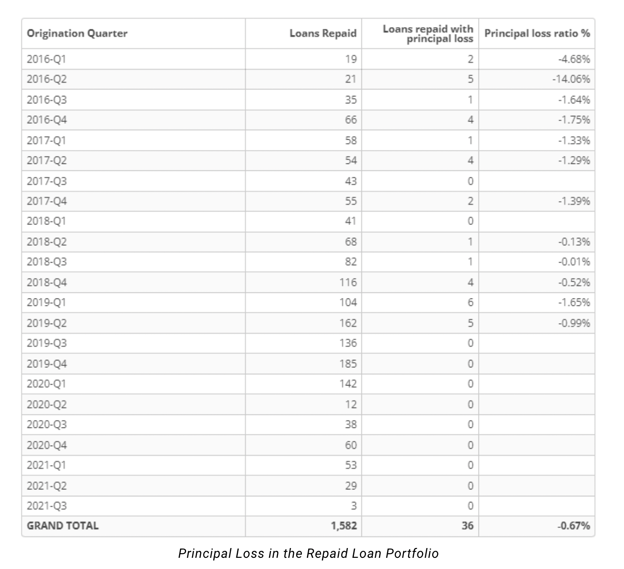

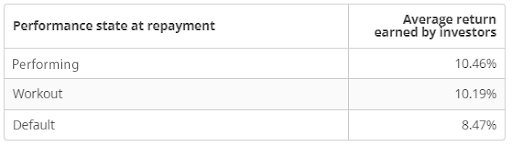

In aggregate, of the 1,582 loans that have repaid since 2016, approximately 62% have repaid while in a state of Performing, 16% from a state of Workout, 20% from a state of Default, and 2% through the sale of an REO property. As we have advised previously, though, workouts and defaults are not necessarily an indication of an impending principal loss. The analysis below shows that of the 1,582 repaid loans represented in the chart above, only 36 have resulted in a loss of invested principal – and the loss ratio resulting from those repayments (i.e. the total principal loss, expressed as a percentage of total principal invested) was only 0.7%.

Newer investors to our platform may be surprised to learn that investing in Workout or Default loans alone has historically yielded a strong positive interest return, nearly on par with investing in loans that repay from a state of Performing. While that result might seem counterintuitive, it speaks to a fundamental truth about our product: Our loans are well-collateralized and soundly underwritten. Even when loans have gone into forbearance or default, we have historically been able to recover strong interest returns on those loans – that we then pass through to investors.

Active Loans, as of September 30, 2021

Finally, we turn to an analysis of our loans currently outstanding – our active loan portfolio. As we did with repaid loans, we report here on the performance state of our outstanding loans, using the same definitions as above.

Performance States of Loans in Our Active Loan Portfolio

Performance States of Loans in Our Active Loan Portfolio

Redefining Defaults

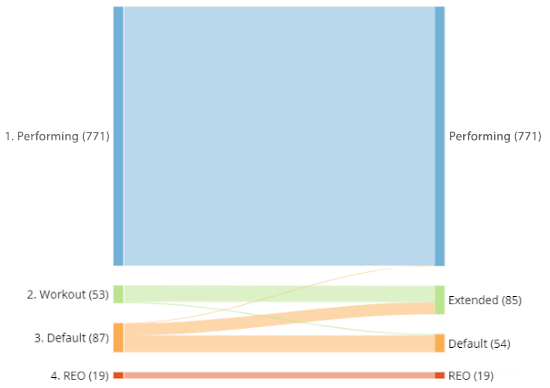

To provide our investors with a clearer picture of portfolio performance and to align Groundfloor with industry standards, today we’re announcing an update and clarification of our categorization of LRO performance states. In the past, we have labeled all LROs for loans past the contract maturity date as “default,” even if the loan was otherwise performing and was expected to repay in full. This label was confusing for investors because “default” did not adequately capture the performance of the underlying loan and did not match the industry definition of defaults against which our performance was inaccurately compared.

Beginning today, loans that pass maturity and are otherwise performing and are expected to repay in full will be classified as “extended” and only loans where legal action is being taken will be classified as “default.” We hope this change will help our investors better anticipate repayments and will make our platform more aligned with the nomenclature used by other investment platforms

Groundfloor has historically labeled LROs as “default” when the borrower has not adhered to one or more terms of the loan agreement, but also if the loan simply passed the maturity date – regardless of whether or not an extension had been granted. This definition of default is much broader than the definition used by our industry peers, who consider a loan in “default” only if investors’ principal is at risk. This is the main reason why loans in the default state on our platform have such a high propensity to repay in full. For example, in Q2 2020, 25% of loans repaid in the default state with zero incidence of loss and with no legal action required on our part to ensure full repayment. Clearly, in many cases the label “default” does not accurately represent the underlying loan performance state when compared to “defaults” on other platforms.

The graphic below illustrates the impact of the classification changes on the composition of our active loan portfolio, with the old states at left and new states at right.

Of course, regardless of the labels, our Asset Management team will continue to monitor loan performance in a proactive manner, working closely with borrowers to ensure that projects stay on track and LROs perform as expected.

We share this kind of information to help support our investors’ success. If you have any questions or comments about this report, do not hesitate to reach out to us. You can comment below or send an email to support@groundfloor.us. We always look forward to hearing from you.