It’s been eight months since our last vintage analysis, and that means eight more months of origination and repayment data to scrutinize. With that in mind, we thought investors would appreciate an update on our asset management and underwriting performance.

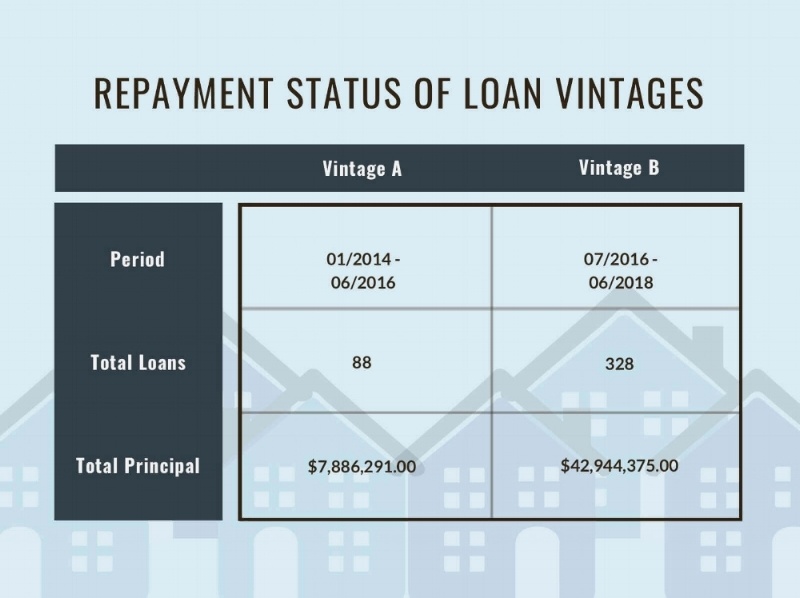

As with our original vintage analysis, we have compared performance for loans originated from January 2014 through June 2016 (Vintage A) with loans originated from July 2016 to June 2018. We exclude loans originated since March 2018 that haven’t yet reached maturity.

Vintages

The repayment status for both vintages is reported and measured as of 8/31/2018, except where noted.

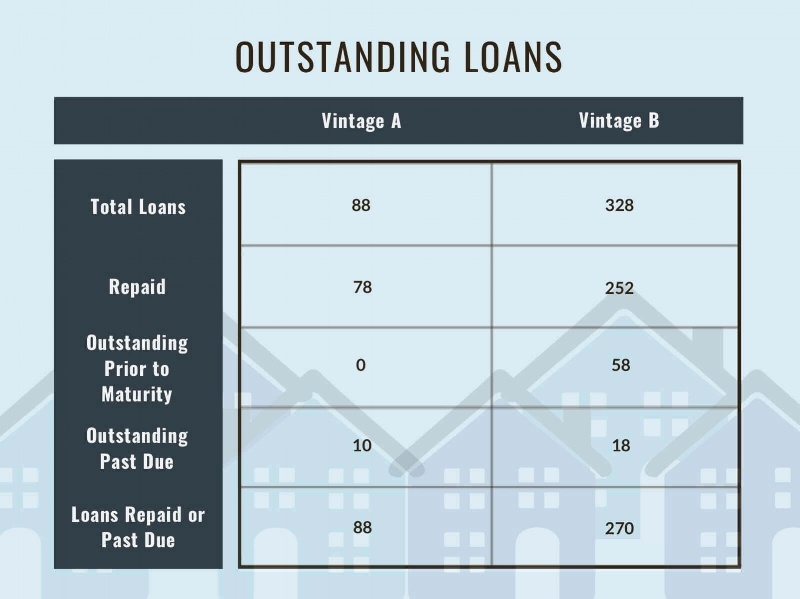

As stated in the original analysis, Vintage A is composed of 88 relatively small, mostly local Atlanta-area loans originated during GROUNDFLOOR’s formative years, a period of 30 months (2.5 years).

Vintage B is composed of 328 loans that were originated following our addition and application of greater lending expertise. This vintage spans 24 months.

Repayment Status of Loan Vintages, as of 8/31/2018

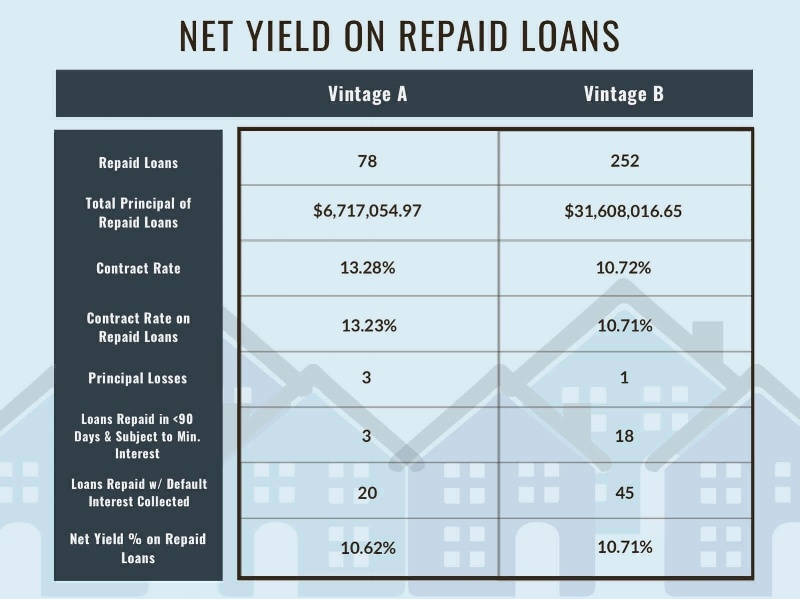

Performance Measure #1: Net Yield (Updated)

First, as we did in the original analysis, we are going to address each vintage’s performance within the context of net yield. Here is a comparison of net yield on repaid loans from Vintage A and Vintage B:

* Contract Rate is calculated as a dollar-weighted average of the contract rate of each loan in the Vintage by principal.

** Net Yield % is calculated as a dollar-weighted average of the actual annualized rate of each loan in the Vintage by principal. The Net Yield calculation includes the cumulative effect of (i) principal losses (negative yield), (ii) minimum interest due and paid on loans of less than 90 days duration and (iii) default interest assessed and collected on loans subject to workout or default.

Net Yield on Repaid Loans, as of 8/31/2018

The difference in contract rate between the vintages is significant. The decrease from Vintage A to Vintage B is partially attributable to the ongoing compression of yields in the lending market we serve. A more important influence, however, has been a strategic choice to pursue the best and most experienced borrowers by decreasing rates over time. We will comment on these dynamics in greater detail in a future post.

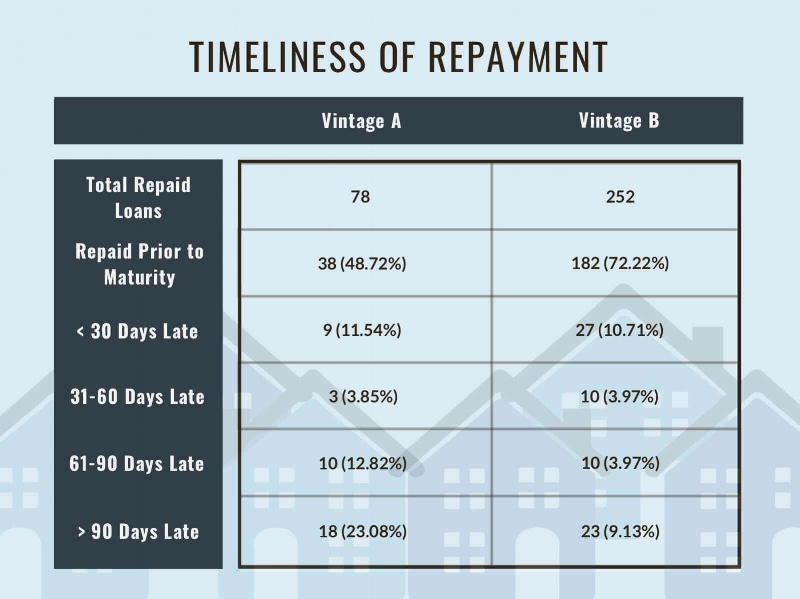

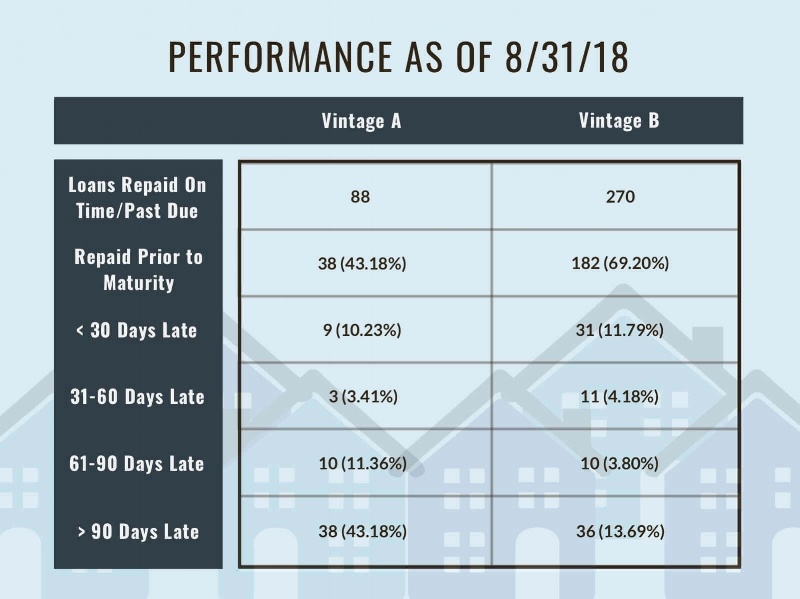

Performance Measure #2: Timeliness of Repayment

In addition to net yield, investors use on-time payment metrics as another indicator of portfolio performance. All Vintage A loans are deferred payment loans, meaning no payment is due until the loan matures, i.e. until its final payment due date. GROUNDFLOOR has recently introduced monthly payment loans as a new product and Vintage B includes a number of these loans.

For each vintage, we analyzed when loans repaid relative to their maturity dates. Here is a comparison of the timeliness of repayment for Vintage A and Vintage B, with percentages provided to break down the share of repaid loans.

Timeliness of Loan Repayment From Each Vintage, as of 8/31/2018

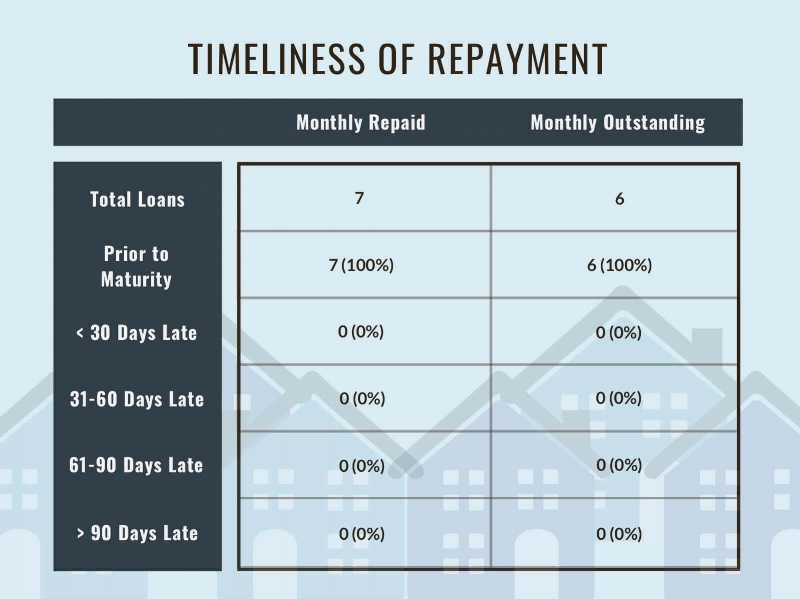

Monthly payment loans are a subset of Vintage B and they have performed well to date, as detailed below.

Timeliness of Loan Repayment of Monthly Loans

In order to gain greater portfolio performance insight, we also analyzed outstanding loans for both vintages. While any outstanding Vintage A loan is clearly delinquent, we wanted to understand the nature of outstanding and delinquent Vintage B loans. Going further, we also re-ran the analysis to include loans that were still outstanding from each vintage as of August 31, 2018. To get the cleanest (toughest) measure possible, we excluded 48 outstanding loans that had not yet reached maturity (no credit for those!), but included 18 that were outstanding but past maturity (because, hey, they’re late!).

Here’s how it breaks down, in summary -- so it’s clear what we’re counting and what we’re not:

The state of outstanding loans in each vintage as of 8/31/2019

The denominator we’re using to assess the current state of our performance, Line 5 above (88 loans repaid or past due for Vintage A and 270 for Vintage B), is:

- Line 2 (78 repaid loans for A and 252 for B) plus

- Line 4 (10 outstanding past due for Vintage A and 18 for Vintage B)

or if you prefer:

- Line 1 (88 total loans for Vintage A and 328 for Vintage B), minus

- Line 3 (no loans outstanding prior to maturity for Vintage A, and 58 for Vintage B), plus

- Line 4 (10 outstanding past due for Vintage A and 18 for Vintage B)

Here is a snapshot of the situation as of August 31, 2018:

Loan Vintage Performance as of 8/31/2018

Findings & Assessment

Our improvements in risk management, underwriting and asset management are making a big difference for GROUNDFLOOR investors. Despite more than doubling the rate of originations, on-time repayment (Repaid Prior to Maturity) for Vintage B exceeds that of Vintage A by 26%, 69.2% vs. 43.2%. Even if every outstanding past due loan in Vintage B went 90 days late or more, which is highly unlikely if theoretically possible, we’d still realize a 11.8% improvement in loans over 90 days late (from 31.8% down to 20.0%).

GROUNDFLOOR’s Asset Management team grew with the addition of Brianne Cunnion, a licensed real estate attorney, and Jake Harley, an experienced mortgage analyst. Importantly, the team continues to enhance and refine its monitoring and default resolution practice. Net yield and repayment timeliness are the most important metrics to a mortgage investor and accordingly are the objectives we seek to maximize. Our proactive default management has resulted in several unusual, yet positive, outcomes for investors, such as selling two REO properties at a profit and getting outbid at two foreclosure sales.

Even more significantly, despite significant growth in origination unit volume, our asset management team has returned capital on 252 loans in Vintage B with only one loan realizing a loss of principal. While we strive to avoid any loss, the realized loss was limited to approximately 5% of the principal.

Conclusion

With eight more months of data in the books, our updated analysis still illustrates the major improvements made, and processes continually improved upon, by our Asset Management and Underwriting teams since 2016.

GROUNDFLOOR was founded to open access for everyone to investments previously available to only a select few. With that in mind, and even as our popularity continues to grow, we are as committed as ever to transparency. We will continue to make improvements in our processes, technology, and policies while sharing data and performance metrics to quantify our progress. You can count on us to continue providing the tools needed to invest in new ways with confidence.

If you have any questions or comments, please leave them in the discussion section below and we'd be pleased to provide clarification and more details!